S&P Global Market Intelligence is excited to present our in-person event, An Era of Change: Navigating Global Disruption & Transformation, in New York City on April 26, 2022.

Big 4 UK banks hike loan loss provisions, with Lloyds most wary of weak economy

Insight Weekly: Energy reforms after midterms; Crisis ends ‘age of gas’; bank deposits fall

Global M&A by the Numbers: Q3 2022

Insight Weekly: Elections to shape recession response; Companies increase efficiencies; UAE’s bad loans

Gauging Potential Inflation Concern in Market Sectors Using Simple Natural Language Processing

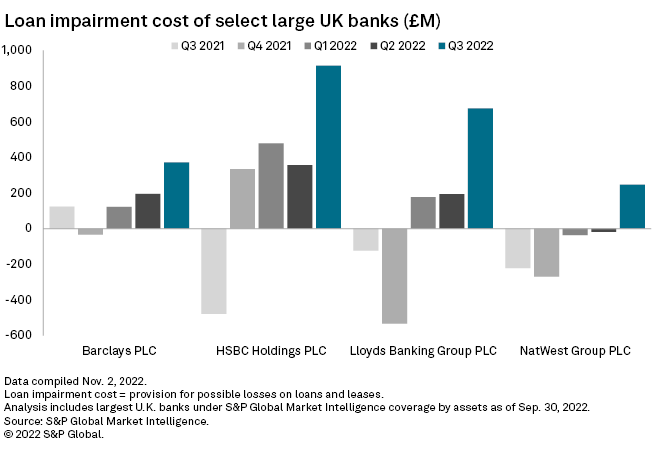

The four largest U.K. banks stepped up loan loss provisioning in the third quarter as they braced for an economic downturn next year, with Lloyds Banking Group PLC booking the biggest increase from a year ago.

An expected sharp fall in housing prices, combined with a surge in unemployment amid weaker growth and a cost of living crunch, prompted Lloyds to ramp up provisions for possible losses in 2023, although asset quality remains strong and the earnings outlook is positive thanks to rising interest rates, CFO William Chalmers said Oct. 27.

Executives at the other three leading U.K. banks — HSBC Holdings PLC, Barclays PLC and NatWest Group PLC — made similar statements.

Impairment costs, reflecting provisions for possible loan losses, at the four U.K. banks increased materially in the third quarter compared to the same period of 2021 and the previous three months, S&P Global Market Intelligence data shows.

NatWest took an impairment charge in the third quarter, versus a release in the second, due to a “more challenging” macroeconomic outlook, but has “not yet seen any material signs of stress from customers,” CEO Alison Rose said during an Oct. 28 earnings call.

HSBC and Barclays, which have larger global businesses and more diversified loan books, are preparing for higher credit losses in the U.K. in 2023. Nonetheless, they expect the benefit from rising rates to help offset an increase in provisions. Barclays’ U.K. business is well positioned to benefit from higher interest rates, which have contributed to “significant” growth in group net interest income, CEO Coimbatore Venkatakrishnan said during an Oct. 26 earnings call.

Profit hit

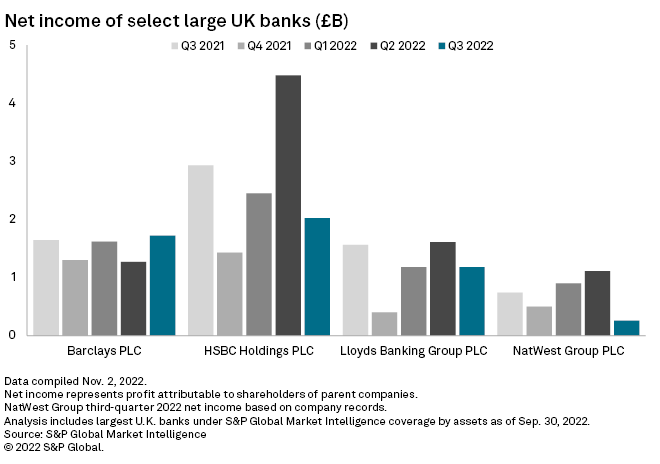

Higher impairments dented profits, with HSBC, Lloyds and NatWest posting a drop in net income both on a year-over-year and quarter-over-quarter basis.

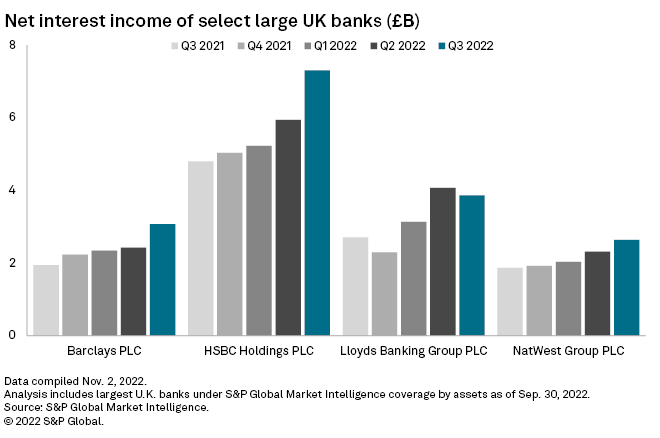

Net interest income was considerably higher than a year ago at all banks, with Barclays and HSBC both booking year-over-year growth of more than 50%.

Banks and market observers expect higher interest rates to be the main future driver for U.K.-based revenues, even though rate hikes have triggered a jump in mortgage rates and fueled concerns about consumer affordability. Lloyds, which holds the largest share of the U.K. residential mortgage market, remains upbeat in its outlook, although repricing in its book has already started.

“The tailwinds are outweighing the headwinds,” CFO Chalmers said.

Analysts at investment bank Berenberg estimated that Lloyds would see a roughly 1% drop in mortgage lending and flat overall consumer credit lending in 2023. Yet, this “moderate” lending volume headwind would be more than offset by deposit volume growth, which would expand Lloyds’ capacity to earn from its interest rate hedge, the analysts said.

|

* Access provisions data for Lloyds on the CapIQPro platform. * Access aggregate financial highlights for U.K. banks on the CapIQPro platform. |