Getty Images

Roll back a decade and the UK sports market was booming.

BT Sport launched in 2013 and sparked an intense rivalry with Sky which saw the total value of sports rights spend grow by 118 per cent over the next five years to reach UK£3.24 billion (US$3.8 billion) by 2018. This was primarily being driven by competition between the two pay-TV broadcasters, and though many of the larger value deals were concentrated around top-tier sports, the money was trickling down throughout the industry.

However, in the last few years both companies have taken their foot off the gas in relation to sports rights, ostensibly looking to preserve the status quo. The result has been a considerable slowdown in growth – only eight per cent between 2018 and 2021.

This slowdown has also been influenced by a lack of new entrants in the UK sports media market over the past decade. Eleven Sports made a spirited attempt in 2018 with LaLiga and Serie A soccer rights, but it wasn’t until Amazon Prime bought a Premier League package – along with some smaller golf and tennis tournaments – that an over-the-top (OTT) player established multi-year deals with a major sports rights holder.

But since then competition has stagnated. The UK has not seen the shake-up that has been happening in other European markets where the likes of DAZN and Amazon have been growing their sports portfolios. As of 2022, only two per cent of sports rights spend in the UK can be attributed to subscription OTT, compared to 32 per cent in Germany and 52 per cent in Italy.

However, there are changes afoot. Discovery, which holds pan-European rights to the Olympic Games, housing much of the content on its streaming platform Discovery+, has entered into a joint venture with BT Sport. Amazon, meanwhile, has acquired a Uefa Champions League rights package and Viaplay, the entertainment OTT platform from the Nordics, is launching in the UK in the latter half of the year. Then there’s always the possibility of DAZN launching, with rumours of the streaming platform acquiring Indian Premier League (IPL) cricket rights in the UK.

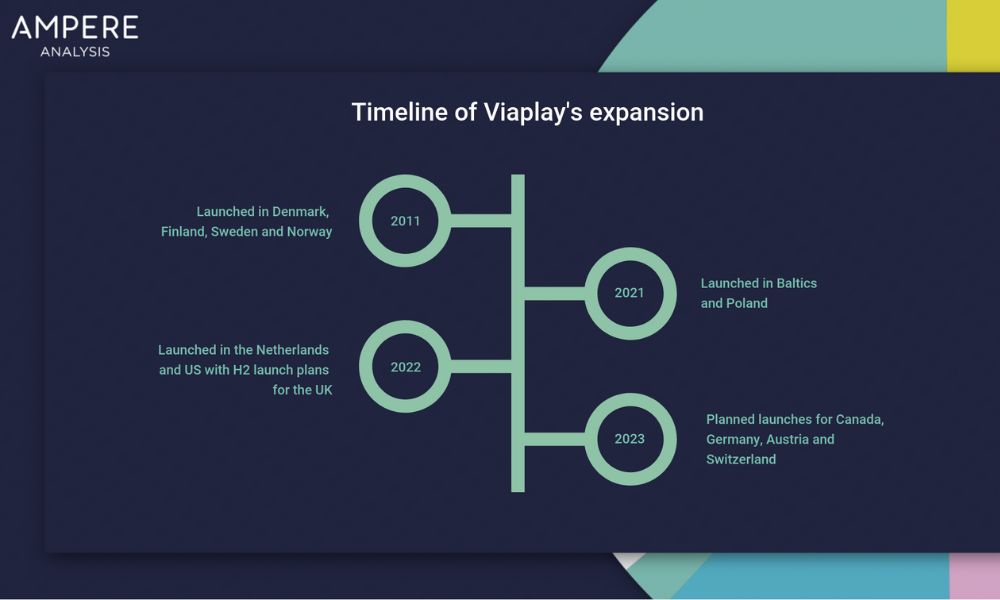

But the big question for now is what impact will Viaplay have? In order to answer that question, we need to look at the platform’s international expansion journey so far:

The strategy in these markets has been to combine entertainment and sport. Across Viaplay’s current European markets, the entertainment element includes popular titles such as The Handmaid’s Tale, The Office (US) and the latest Spider-Man films.

From a sporting perspective, Viaplay has rights to several top-tier properties, including English soccer’s Premier League, Germany’s Bundesliga and Formula One. Given the strength of this offering, Ampere forecasts that by the end of 2022, Viaplay will have a combined 1.95 million subscribers across the Baltics, Poland and the Netherlands and will hit 3.61 million by the end of 2025.

In the UK, Viaplay has chosen a slightly different approach. In July 2022, the company announced its acquisition of Premier Sports, an Ireland-based pay-TV channel which has been broadcasting since 2009. Through this acquisition, Viaplay will gain access to a portfolio of tier two rights including LaLiga, the Scottish Cup soccer tournament and the United Rugby Championship (URC), as well as the Nascar stock car racing series.

The official announcement of the acquisition stated that Premier Sports currently has 220,000 paying subscribers, which provides Viaplay with a solid platform on which to build. In addition, the platform already has carriage deals in place with Sky, Virgin and Amazon. This is important because it will allow Viaplay to tap into sports fans across the spectrum, irrespective of their viewing platform preferences.

Viaplay has also acquired rights to show international soccer games featuring the Scottish, Welsh and Northern Ireland national teams (as well as other European countries), in addition to ice hockey, World Athletics competitions and handball.

But just how attractive are these additional rights to sports fans in the UK?

If we assume that Viaplay will combine the rights currently held by Premier Sports with its newly acquired ones, there is obviously going to be some overlap in interest. Through Ampere’s Sport Consumer data, we can deduce that 75 per cent of fans are interested in both Premier Sports’ existing portfolio and Viaplay’s new rights. This leaves just 25 per cent whose interest is being driven by the platform’s new properties and are therefore a new targetable audience.

However, given that Premier Sports will not have converted all of those who are interested in its offering, in reality, the potential target audience is higher.

We can again use Ampere’s Sport Consumer data, to create an addressable audience funnel for sports fans in the UK who would be willing to pay to watch the international soccer competitions (i.e. Viaplay’s major new rights). This shows that 3.4 per cent of sports fans would be willing to pay, which equates to approximately 364,000 subscribers. If we assume that roughly 40 per cent of them will be targetable, this brings the number down to 145,600 potential additional subscribers.

In the Netherlands, a Viaplay subscription is priced at €9.99 per month. If we loosely assume the price will be a little lower in the UK to account for lower-tier sports rights – i.e. UK£7.99 (US$9.41) per month – and Viaplay is able to convert all of the potential additional subscribers, it would make in the region of UK£1.2 million (US$1.4 million) per month.

There are of course other factors which will bring this number up: Viaplay offers a viable OTT platform through which to watch and the service includes entertainment as well as sport, making it appealing to a wider audience. Despite this, Viaplay will still need to invest in more premium rights if it wants to attract a larger cohort of UK sport fans.

While its current set of rights in the UK are not top tier yet, Viaplay’s strategy in other European markets suggests that tier one properties are an essential part of the proposition. This can only be a good thing for the wider UK sports media market.

Currently, Ampere forecasts that sports rights spend in the UK will decline by ten per cent by 2024. However, if Viaplay’s European model is replicated here, it will create further competition for rights and, in theory, increase the overall value of the UK sports market.

In addition, 67 per cent of sports fans in the UK currently either actively want to watch live sport via OTT or don’t mind the platform they watch on. Viaplay’s entrance in the market will serve these fans and provide them with an additional online option.

However, replicating its European strategy in the UK could see Viaplay’s spend concentrated primarily on tier one properties. This would obviously be beneficial for those rights holders who are already taking the lion’s share of revenue in the market, but may not trickle down to tier two or three leagues for whom competition for their rights is crucial to their future.

But if Viaplay’s content spend in the UK does stack up, one thing is for sure – it will shake up the status quo and truly test Sky and BT/Discovery’s resolve in their sport investments.

You’ve reached your article limit for this month. Please create a free account to continue enjoying our content.

Have an account? Log in

A link has been emailed to you – check your inbox.

Already registered?

Don’t have an account?